How to jam a buyer

Examples of things a seller could do to rake you over the coals

Back in college, one of my professors spent a week teaching us how to commit accounting fraud. He covered everything from skimming the till, to creating phony financial statements. He believed that understanding how fraud happens in the real world is more useful to an auditor than simply learning a bunch of rote procedures. I think that was a good approach.

In all of my financial due diligence engagements, I never encountered a case of fraud. I saw plenty of errors but most of those were just plain mistakes and not malfeasance. I did once encounter a seller with a second family running through the company payroll. That is not accounting fraud though. His business, his money.

He was upfront about it. All of the details were open to potential buyers. All he asked for was an EBITDA addback since it was non-operating in nature along with our discretion.

The sellers that I have encountered have largely been honest and hard-working folks. An M&A deal presents about as much information asymmetry as one could imagine though. This is an opportunity for a seller to take advantage of a buyer. Thus no matter how much trust and rapport is built, the best approach is buyer beware.

As such, I think it would be helpful to present a few ways in which a seller might actually do this. Like my accounting professor’s approach, I think that showing you the dark side might be more useful in avoiding a landmine than simply giving you a list of diligence questions.

I have not seen these examples directly in a deal. They are risks talked through with buyers and sellers during diligence. The best way to cover your ass in a deal is to think of the worst potential scenario and work backward probabilistically. As you read these, you might find them silly and think, “I would never fall for that”. Maybe not.

You would be surprised though at how often things like this just fall through the cracks as errors and are discoveries after closing. Now think about easy it would be for someone with all the information to fool you on purpose.

To that end, here are some ways a seller could jam you:

1. Creating income via change in accounting principle: One of the easiest ways a seller may fool you is by simply changing one of assumptions they make in arriving at the reported numbers. One example of this is the allowance for doubtful accounts or bad debt reserve.

The table below presents a typical accounts receivable aging along with an allowance for doubtful accounts. In the initial total column, the aging aggregates the individual customer balances to arrive at Gross Receivables and then applies a bad debt reserve of 5% of the gross balance (completely made up for sake of example). A company could calculate their reserve any number of ways but the important thing is that it should be generally consistent from year to year.

If a seller wanted to create income, one way they could do it would be to lower the reserve percentage, releasing income into the P&L. The second total column illustrates the net AR balance if the company revised their allowance to 2% of gross accounts receivable.

Changing this assumption results in a revised net receivables balance. The journal entry to arrive there results in a $17 benefit to the P&L.

During diligence, it can hard to spot changes like this on the face of the financials. If your target does an annual audit there will likely be a footnote describing changes in accounting principle. This is uncommon in the middle market though. You are more likely to find a messy GL that buries items like these in “Other Income”. Your best bet is to request general ledger details for large accounts like Accounts Receivable, Accounts Payable, Fixed Assets, Accrued Expenses, etc. and just dig in.

It can make for tedious work but I always request the general ledger at a transaction or journal entry level. The transaction level detail will show you all debits and credits within a set of financials for a given time period. This allows you to sleuth your own answers without having to funnel questions through the accounting department. You can also scan for any entries that appear to be judgmental or non-operating.

2. Gaming the closing around timing of processes like payroll, check runs etc.: These can be hiding in plain sight. It’s common for experienced buyers to slip here.

Companies generally compile financial statements at month, quarter, or year-end. These financials feed your diligence analyses like QoE, NWC, etc. and inform the numbers in your purchase documents. One way a seller could try to game you is by closing the transaction at a different point during the month. Said another way, the balance sheet at mid-month could be significantly different from month-end. If not correctly contemplated in your closing mechanism, you could be holding the bag.

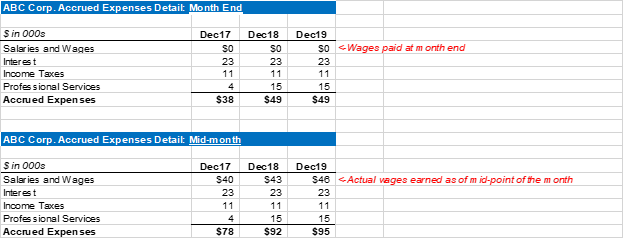

An example of this is accrued payroll. Imagine that our imaginary target pays employees once a month, on the 31st, for work performed through that payroll date. On the month-end financials, accrued payroll will be $0 because there is no outstanding liability at that time. Employees will accrue wages beginning on the next day and receive their check on the next month-end. This cycle drives growth in the accrued balance throughout the month until it is relieved on payday.

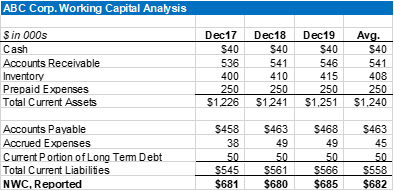

Now imagine that you are calculating a working capital target. The seller has provided you with a clean set of financials (prepared as of month-end) for the last several years. Great data! That may look similar to the following table:

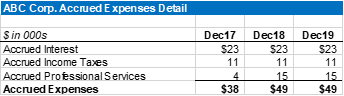

As a part of your diligence, you did a detailed walkthrough of the month-end balances and requested a breakdown of each account. Your detail of accrued expenses might look like the below:

Everything here looks reasonable. In our example, you and the seller might agree that an average of the previous three years NWC, Reported, or $682 is a reasonable target. In your purchase agreement, you might be so thorough as to define accrued expenses as including accrued interest, accrued income taxes, and accrued professional services. Now you’re all set to close…

A few weeks before closing the seller asks you to move the closing up to the 15th. They want to go on vacation with their family and this better aligns with their schedule. In the interest of being a good principal, you agree.

Your problem now is that that the balance of accrued expenses on the 15th of the month is very different from the 31st and you missed it. The table below shows an example. Month-end accrued expenses is $49. Mid-month is $95.

The expense here would be on your dime either way. Had you flagged this in diligence though you would have included accrued salaries and wages in the definition of net working capital in the purchase agreement and at settlement, the true-up mechanism would reflect that the amount delivered was lower than the target. This would result in a credit to you for the difference. Without including it in the definition, you would have to eat the $46.

You could ask all the right questions here and still miss it. You asked the seller for a detailed break down at 12/31 and they showed it to you.

The key to finding things like this is to step back and talk about processes vs. financial results. Discuss how $1 moves through the working capital cycle. Take a calendar and just markup important days of the month. Examples of this would be payroll runs, debt service payments, when the company cuts checks, etc.

3. Hanging expenses up on the balance sheet – If I wanted to fool somebody, this would be the way.

In item #1, I talked about how someone might use reserves to create phony income. The other way to use the balance sheet is to hang expenses up via capitalization so that you delay their recognition for as long as possible.

When you capitalize something to the balance sheet, you push the accounting recognition of the cost over future periods. The business takes the cash hit but the P&L impact leaks out in dribs and drabs that appear much less costly from month to month.

This fib relies solely on buyer inexperience. It’s a gamble that you’ll just miss it. If you’re not an accountant or not willing to pay one to help you they are easy to gloss over.

One way a company might do this is by simply fluffing up the name of the expense to sound more reasonable. “Marketing expense” might be “capitalized customer acquisition”. Payroll for a fleet manager may be “fixed assets administration” etc. hoping that you hear “fixed assets” and just move on.

Another way a company could defer expenses is by just being aggressive with items that could go either way. Said another way, when something is a toss-up between expense vs. capitalize a company might just always defer to capitalization.

Most companies have a monetary threshold above which they capitalize expenses, say $5,000. If a cost is less than the threshold they expense it. If more, it is capitalized.

A company could be aggressive and just set the bar at $2,500. Ceteris paribus, this would push more dollars to the balance sheet to trickle out over time vs. hitting COGS or SG&A in the period of purchase.

These are just three examples of items to keep in mind as you go through diligence. The best way to stay out of trouble is to look at as many businesses as you can and just get more repetitions. The more companies and deals you see, the more reference points you have.

These form a latticework to frame your overall diligence approach. You’ll then have a better idea of where to dig when you hear the seller say something odd or perhaps you see something in the numbers that just doesn’t make sense.

Matt. This was incredibly helpful. Recently went into due diligence on a business that had an interesting 'other income' item. I wish I was the one that spotted it, but it was actually my partner. Turns out it was a one time business grant from the UK government.