Calculating Working Capital

An approach to calculating NWC with exhibits and specific numbers

One of the most complicated parts of closing a deal is calculating the Net Working Capital (“NWC”) target and settlement. In recent years, NWC has become an opportunity for buyers and sellers to take advantage of each other through asymmetric information or legalese. All of this can make calculating the target one of the most tedious tasks of any deal.

This is meant to help anyone approaching NWC for the first time or wanting to brush up a little. It’s framed from a buyer’s perspective but hopefully could be useful to either side.

Why is a NWC settlement even necessary?

Confusion often arises from a fundamental misunderstanding of why a NWC mechanism is necessary in a deal. I like to use the following example in discussions with sellers:

If you think of your business as a car, working capital is the gasoline. At this point in the deal, I’ve decided that I want to buy your car and we’ve settled on a purchase price. The next step is for us to figure out how much gas should be in the tank when I drive your car off the lot.

It’s in the seller’s interest for the tank to be as low as possible. As the buyer, I would love for the tank to be full. Together we should analyze the needs of the business and identify what a normal level of “gas” should be. Normal for a Hummer isn’t normal for a Prius.

What makes buying a business more complicated is the number of items that impact working capital at once. In our example of buying the car, you can easily look at the fuel gauge to see how much gas is in the tank at closing. In a business, the constant fluctuation of accounts make it far too difficult to accurately calculate the level of NWC at closing. Inventory is in transit, vendor checks are in the mail, receipts are being processed, etc. all at the exact same time.

For this reason, parties usually wait for a period, typically 90-120 days after closing, and after the dust has settled they will look back and calculate the amount of NWC that was actually delivered at close.

Now let’s go back to our example of buying a car. Say that we have agreed that a half a tank is a normal level. After the lookback period is over and we find out that you have given me three fourths of a tank, I will give you some additional purchase price for the difference. If we find out that you have only given me a quarter tank, you will agree to top me off.

The key takeaway here is that the actual settlement payment from one party to another is only a true up to economics that were previously agreed upon. Often buyers and sellers mistakenly see the settlement payment as winning or losing.

Another way to think about it is this: principals on either side of a deal can do a poor job of negotiating NWC and still get a settlement payment or vice versa.

Why is setting the NWC target so complicated?

Most complexity in setting a NWC target arises from one of the following questions. Each is an opportunity for disagreement that can significantly slow down or halt progress toward completion of a deal:

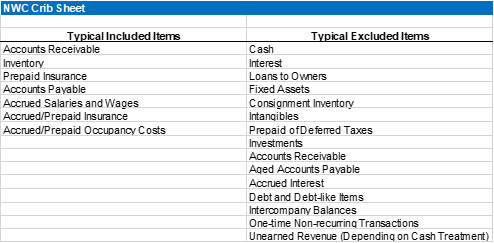

1. What items should be included or excluded from the calculation of NWC?

2. How should we quantify the items that we have agreed should be included or excluded?

3. What time-period offers the best view of a normal level of working capital?

What items/accounts should be included or excluded from the calculation of NWC?

In any given deal, 80%-90% of the items to be included/excluded are “no brainers” or items that never present cause for disagreement. These are usually items like fixed assets or intangibles. The problem is that the other 10% - 20% of accounts that comprise the balance are open to interpretation.

Keep in mind here that smart people can disagree. For that reason, calculating the NWC target is an art as well as a science. Hard numbers feed into the final calculations but there are always exceptions.

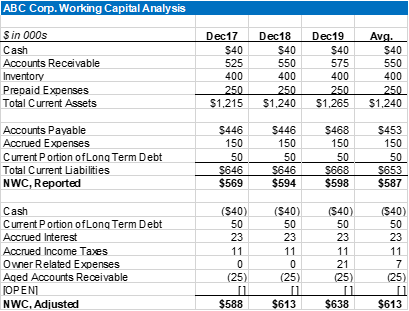

The exhibit below illustrates the way that I start a working capital analysis (note: all numbers here are completely made up). I begin with numbers that are commonly agreed by buyer and seller. Typically, this is the seller’s reported balance sheet. You want to start with reported numbers here because inevitably some disagreement will arise. If you start with the seller’s reported numbers and make adjustments from there, it is easier to bridge the gap and discuss the specific points of difference.

We will work from here to flesh out our view of normalized NWC or NWC, Adjusted.

Consider two items included in the definition of NWC, Reported - Cash and Current Portion of Long Term Debt. Most transactions close on a “cash-free/debt-free basis”, meaning that the economics of the deal reflect the business as if the seller took all cash from the business at closing and retired all outstanding debt. This does not necessarily mean that those actions occur at closing but the economics of the deal are premised on it.

This is beneficial for the seller when evaluating offers from multiple bidders who may have varying views on things like pro-forma debt and how much cash should remain in the business.

Buyers also prefer to look at deals this way because their cost of capital and debt structure may likely be different from the seller’s. As such, their valuation should be based on an expected earnings stream that reflects those differences.

The key takeaway here is that your approach to setting your NWC should be consistent with the overall approach to structuring a deal. Many buyers get into trouble by approaching each stage of the deal as a standalone work stream. Your approach to valuation, structure, NWC, etc. should be approached holistically and consistently.

In this case, to align with our “cash free/debt free” offer we will adjust for the impact of cash and debt in NWC.

The process becomes harder as we move into areas that require a higher degree of judgment. These adjustments may not be taken directly from the face of the financial statements. Rather, they typically require some digging to find, usually through detailed discussions with the seller at a trial balance level.

A common place to start the discussion is with accrued expenses - items incurred by the company but not paid. A great example of this is accrued salaries and wages.

I would start by discussing the company’s payroll process with the seller. That might inform me that month end falls on a Friday but employees were paid the previous Wednesday. If your financial statements are prepared through Friday, they should reflect two additional workdays earned by employees during that month but not paid until the following payroll run. My follow up question to the seller would be if they accrued for them. If the answer here was “no”, an adjustment is necessary.

Another way to identify these, beyond a process walkthrough is to request a more detailed breakdown of accrued expenses from the company. The type of data available will vary from company to company but something like the below is typical. Always remember to agree the detail to the balance sheet feeding your NWC analysis.

In our imaginary deal here, the valuation is based on a multiple of Adjusted EBITDA. Since this excludes interest expense and taxes, we should make adjustments for those when calculating NWC. See the table below for mechanics.

Most potential adjustments kick out when you notice trends or activity in a particular account that just seem odd. Candidly, you’ll just get better about sensing what is odd as you get more deal reps. You’ll also learn that businesses just account for different items in different ways and most of this activity will have a perfectly valid explanation. Occasionally you will find an error, which should result in an easy conversation and correction. Your job here is simply to ask the question and learn the answer. More common in smaller deals, you will come across items that are neither right nor wrong but just the result of how the seller chooses to run things. Personal and owner related expenses in the business are usually the most common occurrence.

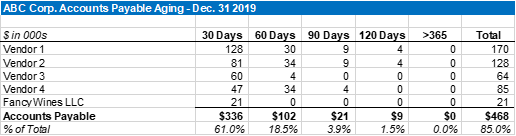

In the summary table above, notice how Accounts Payable seems to increase in Dec19 when it’s been steady for the previous two years. This would suggest that we should dig a little deeper and ask for a detail of the account. This would normally come in the form of an Accounts Payable Aging similar to the below:

Upon examination of the detail, one vendor appears to be very different from the others. In this instance, you may have gleaned from previous steak dinners with the seller that they are an aficionado of fine wine. This is enough information to ask the question about whether this is business related or not.

Christmas gifts to employees or select customers may pass the operational vs. non-operational test but in this case, we would ask the questions anyway. In our imaginary deal, the seller might tell us that they are purely personal purchases that were paid through the business. As such, we should consider them non-operating in nature and an adjustment to NWC.

Key takeaway here: expenses that are personal in nature are not right or wrong. They may inform our opinion of the sellers’ general level of business hygiene but it’s their business and they can run it how they wish. The best way to approach these items is in a non-judgmental way.

How should we quantify the items that we have decided should be included/excluded?

There may be accounts that are clear in their classification of inclusion in NWC but they may still require additional adjustment to quantify how much. Take accounts receivable for instance. There’s no doubt that AR is a part of NWC, but should all of it be?

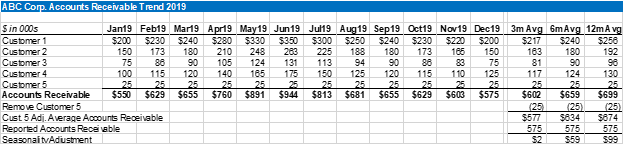

Notice in our summary NWC table above that Accounts Receivable has been growing over the past few years. If the business has been growing, this may be expected but imagine in this case that business is relatively stable. In order to identify what may be going on in Accounts Receivable we might ask for an Accounts Receivable Aging similar to the below:

An Accounts Receivable Aging report gives us a view of how old the outstanding receivables are. Generally, the older the receivable the more questionable its collectability. It’s a great idea to ask for an Inventory Aging report as well which may give insight as to which products are moving and which products are languishing on the warehouse shelves.

In this Accounts Receivable Aging, we can see that Customer 5 has a balance that has been outstanding for over a year when other customers seem to be paying on time. As with the items flagged before, this should be brought up to the seller in a non-judgmental way to get a better understanding of the reason for the aged receivable and whether or not it’s collectable.

It’s not uncommon for businesses to get behind in cleaning up things like this, especially in smaller companies that may be less sophisticated. Again, it’s not right or wrong but simply the way they do things.

In a larger business, someone may review receivables regularly for items that may need to be written off. Here let’s assume that the owner tells you that this customer has been in financial straits for some time and that this receivable has actually been sitting on the books since 2017 and is likely uncollectable.

Based on this explanation, this portion of the overall accounts receivable balance should be excluded from NWC, Adjusted. As such, we adjust for it in our calculation below.

One final point to make here is that often you will identify items which impact several different work streams. Here, if we exclude this receivable from our calculation of NWC, Adjusted, it’s also appropriate to reflect the impact in our calculation of Adjusted EBITDA in the time period it was originally recorded. In this case, a negative adjustment of $25 should ding the 2017 P&L.

What time-period offers the best view of a normal level of working capital?

Our final complication here is the consideration of what time period accurately reflects the working capital needs of the business.

One component of this is seasonality within a given year. Large retailers for example have inventory balances that swell ahead of major holidays. Growth within a particular business may have led to increased sales. This would likely drive higher inventory purchases and payables to service it. In this case, you would likely see growing receivables on the other side.

The overall goal of our diligence here is to inform a view on the amount of working capital necessary to service the needs of the businesses cash conversion cycle post-transaction. The best way to do this is to consider each component of working capital and it’s associated timing in addition to the overall working capital trend.

This approach will ensure that you really understand the mechanics of the cash conversion cycle and how a company transforms cash flow out into cash flow coming in.

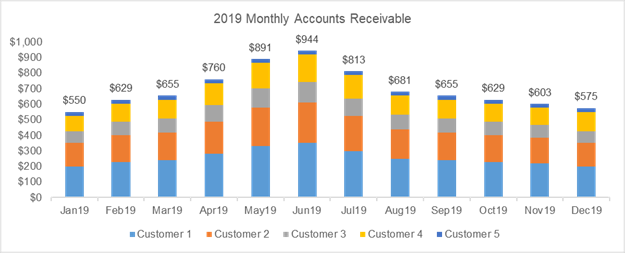

At this stage of the analysis, it’s best to look at the components on a monthly basis if possible. Varying levels of sophistication impact what data is available but if possible, a good place to start would be a monthly detail of Accounts Receivable. This would look similar to the below:

We can see from the table that there is a swell in accounts receivable during the summer.

This trend would tell us that an adjustment is likely necessary to reflect the seasonality of working capital. Often, buyers default to a yearly average. This would be more appropriate than the reporting Dec19 balance but we likely need to analyze further to determine the time-period over which an average would make sense.

Recall from our discussions with the seller that Customer 5 is likely uncollectable, thus we should remove its impact from the analysis. Next we examine the average level of receivables over the past three, six, and twelve month periods in order to get a view of the average levels at various points in time.

In our imaginary deal, suppose that we have discussed the upcoming working capital needs of the business and agree that an average of the last six months is appropriate as it reflects the likely working capital need post-transaction and enough runway before the summer build.

I would then compare this average to the reported amount to arrive at an adjustment for seasonality in accounts receivable.

Your AR seasonality analysis should accompany similar work on other large working capital items such as inventory or accounts payable to better understand the interplay between them as dollars work through the cash conversion cycle. On larger deals, it is typical to analyze working capital on a monthly basis for all accounts in order to get a view on the entire working capital trend. The ability to perform analyses at this level of detail may not be available on smaller deals.

One other important consideration is that seasonality is often considered from an inter-month standpoint, i.e., how does the balance trend from month-end to month-end? Within any given month though, working capital needs can vary greatly from the month-end reported balance due to the timing of large expenses like payroll, batched inventory purchases, or AP payments.

It’s important to spend some time with the seller discussing these inter-month needs to make sure you don’t miss large items that could surprise you post-deal.

It's also important to make sure your closing date timing mirrors the reporting dates used in your working capital analysis. For example, if you set your target based off month-end balances but decide to close on the 15th someone may be surprised when a large payroll run or other bill is due.

How do we come to agreement with the seller?

Performing an analysis of working capital can take a lot of work but if you can’t come to terms with the seller in a productive way all that work may be for naught. I’ve found that the following steps are key in making the discussion around NWC as smooth as possible.

1. Agree on approach first – The foundation for success is placed when framing the LOI which should include the broad strokes of a NWC mechanism. The key here is to avoid surprises and the best way to avoid those is through regular discussion along the way. Your LOI plants the seed.

As diligence proceeds, the next step is a detailed discussion on approach. This conversation should note the data that you will look at and analyses you will perform. The aim of this conversation is to get on the same page and to that end, I find it helpful to leave out the numbers. This allows you to narrow your focus to the “what” and the “why”. Subsequent conversations will address the “how much”. A few typical items that you may note to the seller are below

2. Schedule an extended due diligence session and show up prepared – Your general request list should be detailed enough and include items sufficient to form a preliminary view on working capital before your first detailed discussion. This includes an Accounts Receivable Aging, Accounts Payable Aging, Inventory detail by SKU, etc.

These items can be the basis of a detailed discussion about specific components and your thoughts on a quantified amount. It’s best to have a preliminary number fleshed out with a bridge from the seller’s reported financials to a preliminary NWC, Adjusted.

The goal here is to make your discussion around “how much” as substantive as possible and not drawn out. You want to hit bottom on a collaborative answer as soon as possible. Discussions around NWC usually happen in the later stages of the deal and can cause “deal fatigue” like no other. The way to combat this is to have your ducks in a row and don’t waste the sellers time.

These discussions are also an opportunity to build trust and rapport that may be useful in other deal discussions.

It’s also important that your preliminary view on working capital is well thought out, respectful of both sides, and not approached as an opportunity to take advantage of them.

3. Incorporate any findings and changes from the diligence session quickly – In a perfect world, a majority of adjustments in either direction will be agreed to during the preliminary discussion. Any remaining items requiring further analysis are to be wrapped up expeditiously so that you can revert to the seller with final numbers.

With respect to negotiation at this point, it’s best to define all points of contention before attempting to settle any one. This helps prevent the seller from “re-trading” certain items with a never-ending supply of new issues.

4. Shake hands and fill the numbers into the SPA.